Institutional Investors in Single-Family Homes

Evidence from Single-Family REITs

There has been increasing interest from major news outlets regarding “Wall Street” investors in single-family homes. This term is used to describe institutional investors that raise capital either from large private investors, or on the stock market with the aim of purchasing single-family homes, and managing them as rentals. Concerns about the effects of these investors on housing affordability, in particular for first-time buyers, have placed this issue at the forefront of policy discussions. In fact, recent legislation has been proposed to specifically address institutions investing in single-family homes.[1]

In this post, drawing from a recent paper[2] on the topic, we highlight some key facts about one the most specialized and important groups of Wall Street investors: Single-Family REITs. We focus on their growth over time and on the characteristics of the neighborhoods in which they concentrate their investments.

A REIT (Real Estate Investment Trust) is a corporation that acquires, manages, and develops real estate properties, or holds related mortgage loans. Typically, REITs function as large-scale landlords of commercial properties, with rents being their primary source of revenue. Many of the largest REITs are publicly traded on major exchanges, such as the New York Stock Exchange, and attract a diverse range of investors, including individuals, pension funds, foundations, insurance companies, and so on. Single-Family REITs, in particular, specialize in managing large portfolios of single-family homes as landlords.

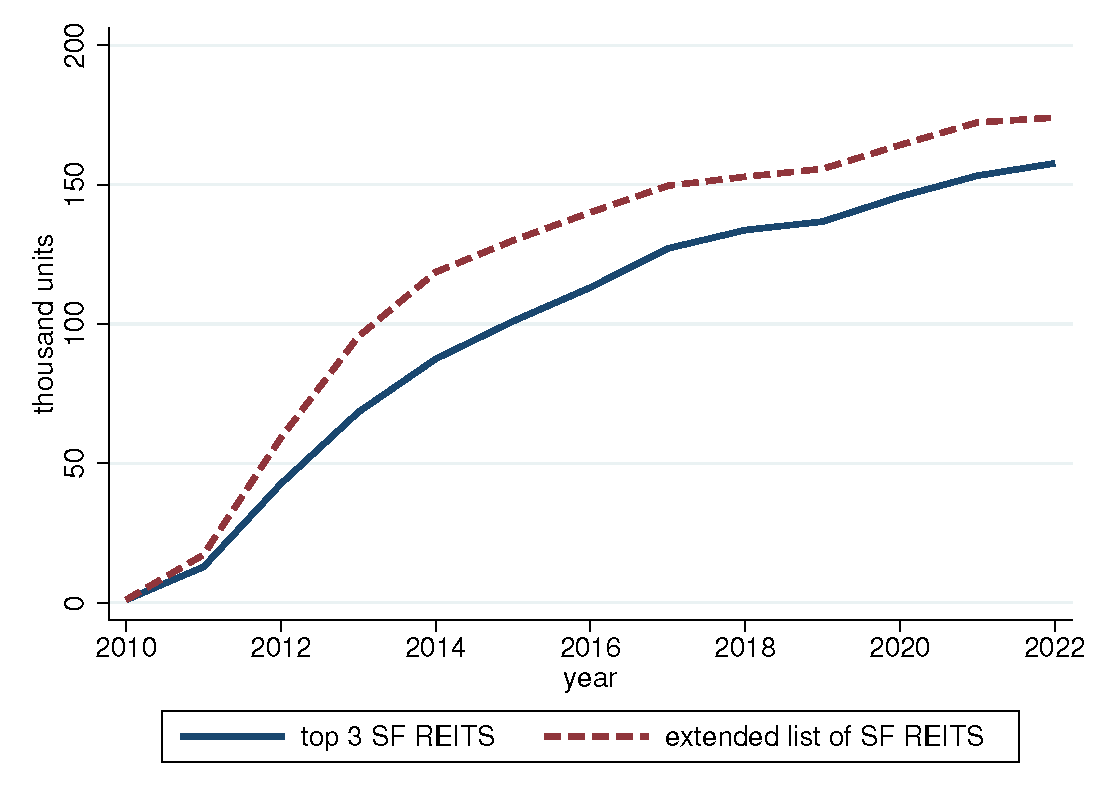

The graph below shows the increase in the total number of single-family homes owned by Single-Family REITs, between 2010, when these investors entered the housing market, and 2022. We show separately the holdings of the top-3 largest REITs (Invitation Homes, American Homes for Rent, and Tricon), and the holdings of all Single-Family REITs in the US. There is a steep increase between 2012 and 2018. By 2022, Single-Family REITs owned approximately 175,000 homes. While this is certainly a large number, it is only a small fraction (0.4%) of the entire stock of single-family homes in the US.

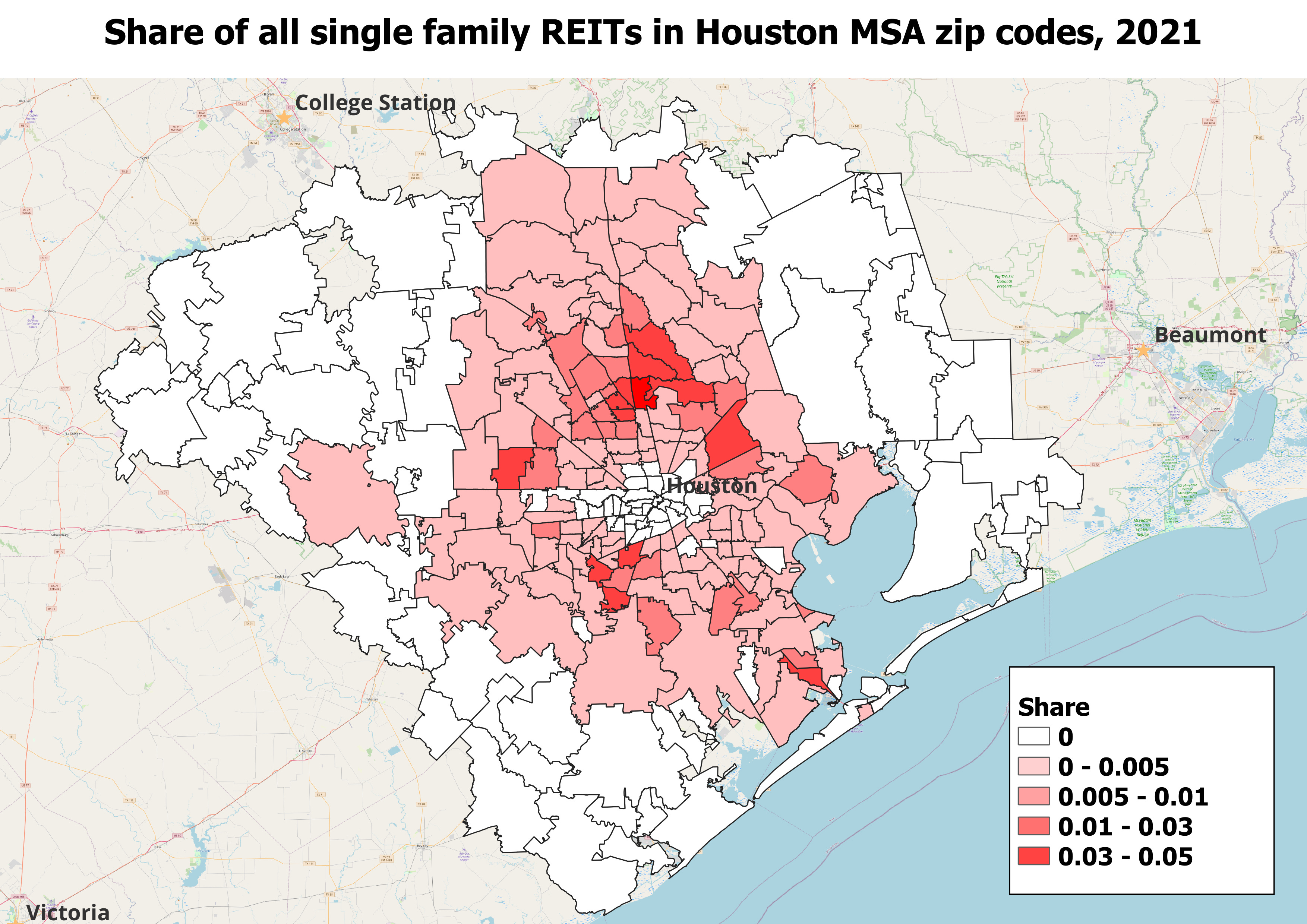

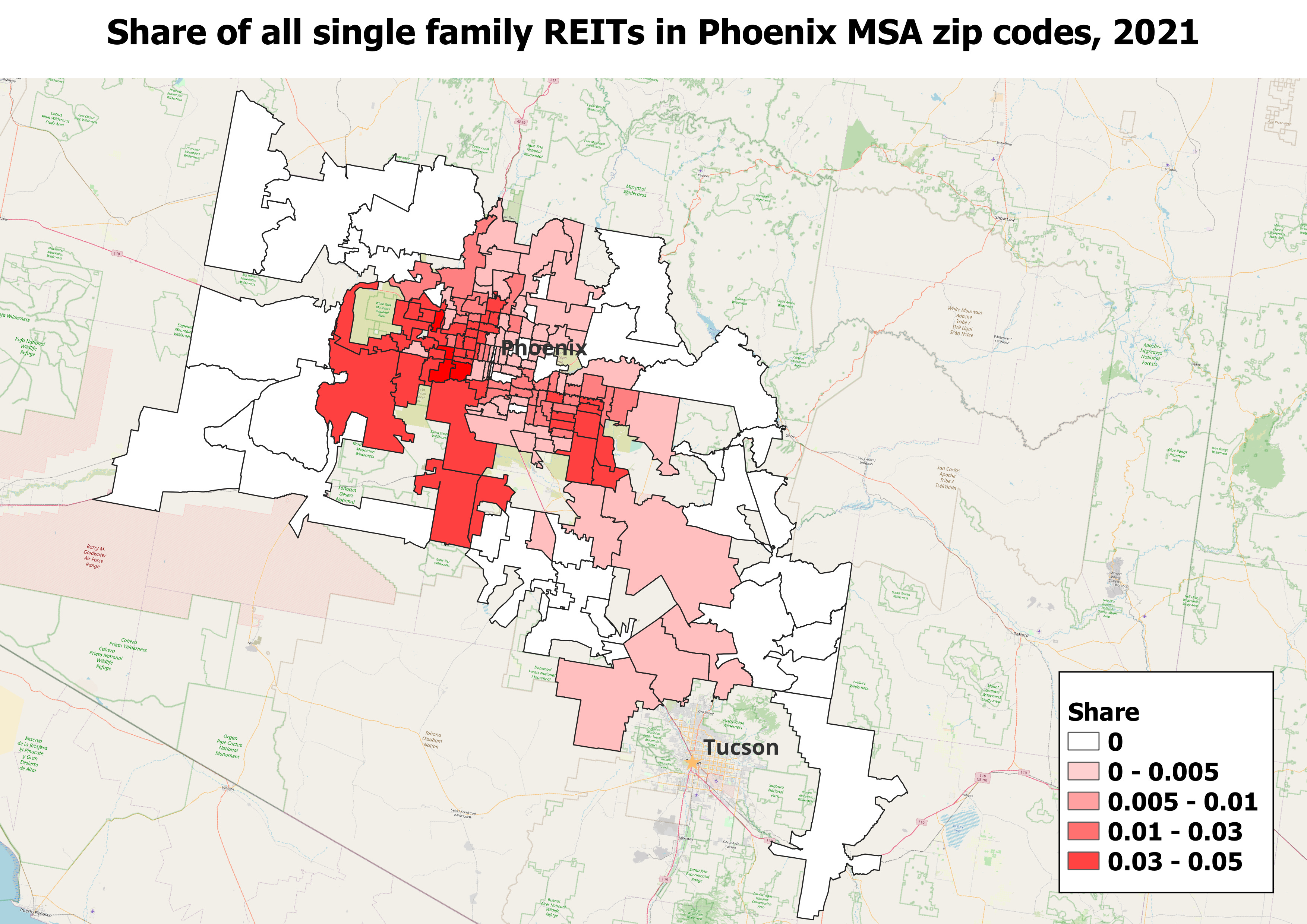

However, these holdings are not evenly spread across the US, or even within cities. Most of the properties owned by single-family REITs are concentrated in large cities in Arizona, Florida, Georgia, North Carolina, and Texas. And even within these cities, Single-Family REITs target specific zip codes.

As an example, the figures below display the share of Single-Family REITs holdings, as a fraction of all single-family homes, in each zip code of Atlanta, Houston, and Phoenix. REITs properties are concentrated in a ring, located between the downtown area and the outer suburbs. This pattern is not limited to these three cities but is common across all the main metropolitan areas in which Single-Family REITs operate.

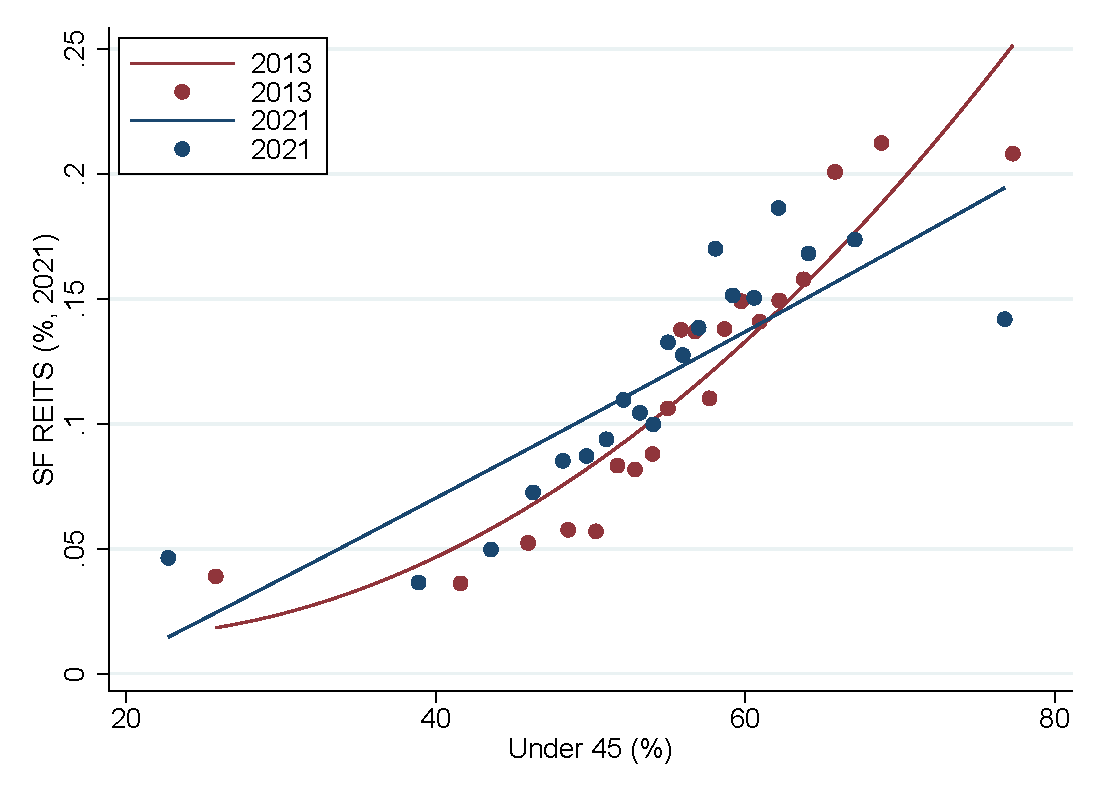

This concentration occurs because housing demand and supply in these mid-town neighborhoods possess characteristics that are particularly attractive to REITs, as illustrated in the figures below.

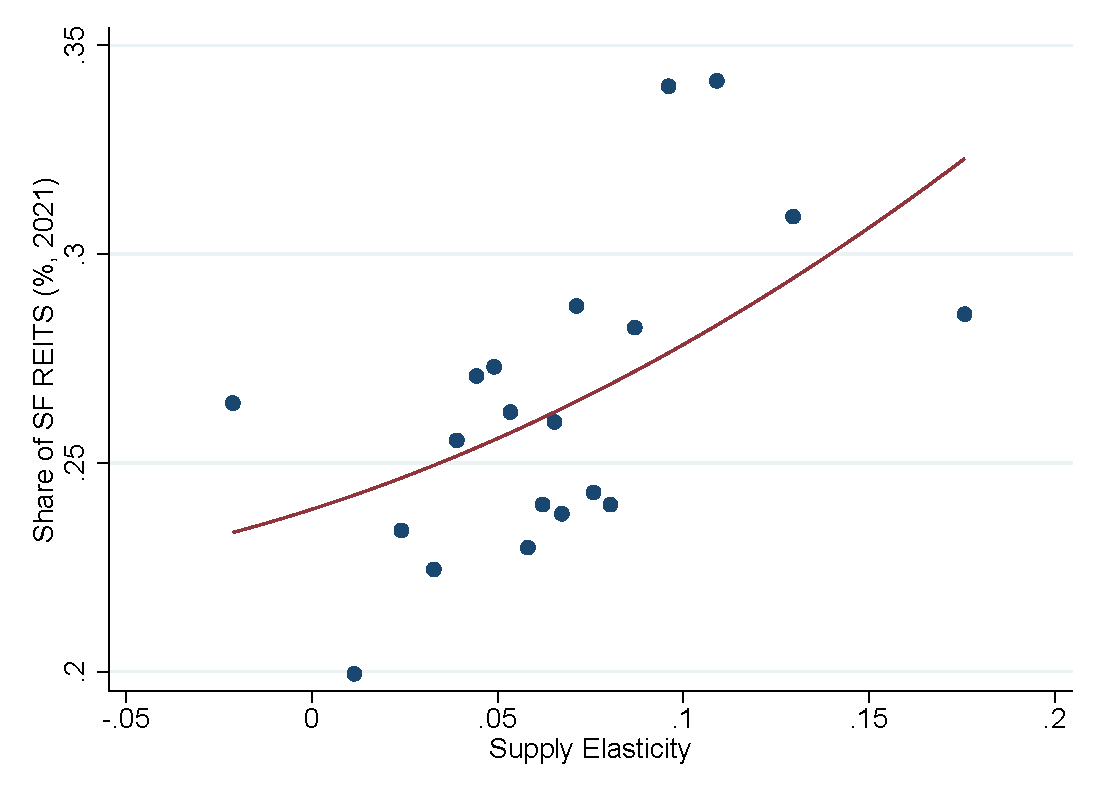

The figures show the relationship between the share of single-family homes owned by REITs in a zip code, and various zip code characteristics, both at the onset of the REITs holdings expansion in 2013, and more recently in 2021.

REITs presence is higher in zip codes that have lower average income (AGI = average gross income), a larger share of minorities, and a larger share of population under 45. These factors are associated with financial constraints that prevent households from entering the ownership market. Moreover, they are associated with demographic growth. Combined, these are indicators of strong demand for rentals.

Moreover, REITs presence is higher in zip codes that have higher “supply elasticity” to prices. These are zip codes in which price increases are more likely to trigger new construction. In other words, REITs enter zip codes in which they can expand their holdings as prices grow.

In addition to highlighting key aspects of Single-Family REITs expansion in the U.S., the facts discussed in this post have important implications for the impact of REITs on local housing markets.

The concentration of Single-Family REITs holdings in specific zip codes increases the likelihood that they will influence local house prices and homebuyers, even though they own only a small share of single-family homes nationally.

However, quantifying the impact of REITs investments on these areas is challenging, exactly because REITs tend to select zip codes with high expected future growth in both demand and supply. In other words, REITs do not invest randomly. They select areas that already possess specific characteristics and trends. As a result, it becomes difficult to separate the effects of REITs from those of pre-existing factors.

The policy discussion should recognize these challenges and exercise caution when linking local market trends to the effects of “Wall Street” investors.

[1] See for example the End Hedge Fund Control of American Homes Act proposed by senator Jeff Merkley.

[2] The views expressed in the paper are solely those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of Philadelphia or the Federal Reserve System. Nothing in the paper should be construed as an endorsement of any organization or its products or services. Any errors or omissions are the responsibility of the authors. No statements should be treated as legal advice